The oil price is approaching a critical point, what will happen in mid-April?

Original Article Title: (WCTW) The Oil Market Breaking Point

Original Article Author: HFI Research

Translation: Peggy, BlockBeats

Editor's Note: This article believes that what truly drives oil prices is not just when the conflict ends, but rather "when the tipping point is crossed".

During the nearly four-week Iran conflict, the oil market is undergoing a typical "time pricing". Strategic reserve releases have delayed the impact but could not eliminate the supply gap; disruptions in oil tanker shipments and lagging capacity restoration have continuously accumulated inventory pressure toward the future. Once past this key mid-April threshold, the price mechanism will shift from "buffered volatility" to "gap-driven repricing".

More notably, the game structure itself is also changing. The conflict is no longer following an "escalation to de-escalation" path but is turning toward endurance testing the market's breaking point. Whoever can hold out until the supply-demand imbalance is priced by the market will have the negotiation leverage. This means that even if the conflict ends in the short term, oil prices will find it difficult to return to their original range. The current supply losses are reshaping the global oil balance for the foreseeable future.

The following is the original article:

In this article, I will break down several scenarios that could currently unfold. With the Iran conflict ongoing for nearly four weeks, how will this situation affect the oil market?

On March 9, we published a public article titled "My Latest Judgment on the Oil and Gas Market Under the Iran Conflict," in which we wrote:

Here are the impacts on oil prices under different scenarios ("barrels lost" already include the time needed to restore capacity):

Scenario One: Oil tanker shipments resume the next day

→ Brent crude's annual average price will be in the range of $70 high to $80 low (approx. a loss of 210 million barrels)

Scenario Two: Oil tanker shipments resume by March 15

→ Brent's annual average price will be in the mid to high $80s (approx. a loss of 290 million barrels)

Scenario Three: Oil tanker shipments resume by March 22

→ Brent's annual average price will be in the low $90s (approx. a loss of 370 million barrels)

Scenario Four: Oil tanker shipments resume by March 29

→ Brent's annual average price will be in the mid to high $90s (approx. a loss of 450 million barrels)

If by March 29, oil tanker shipments still cannot resume normal operations, the situation the oil market will face is almost unimaginable. The only way out will be a forced demand contraction, and prices will also be pushed to extreme levels.

Shortly after the report was released, the International Energy Agency (IEA) announced a coordinated release of a total of 400 million barrels from the global Strategic Petroleum Reserve (SPR). This will partially alleviate the impacts of supply losses. However, as pointed out in our subsequent article "IEA Coordinated SPR Release: The Ultimate Gift to Bulls":

From a trading perspective, traders will not rush to push oil prices higher until this "buffer" is depleted. While the concentrated release from the SPR does help alleviate short-term supply anxieties, it is only a temporary solution. The market will remain tense, and as long as oil tanker shipments do not return to normal for a day, oil prices will gradually rise.

On the other hand, if the situation quickly eases—such as an immediate ceasefire or agreement—oil prices will drop rapidly. For example, if a peace agreement is reached before March 15, global inventories will net increase by 110 million barrels (400 million released - 290 million lost).

This could push Brent prices back towards the $70 middle range.

Conversely, if there is no peace agreement and supply disruptions persist until the end of March, global inventories will net decrease by 50 million barrels, and for each additional week, the gap will widen by approximately 80 million barrels.

Therefore, the role of the SPR is only to "buy time" and does not address the core issue. Oil tanker shipments must return to normal. However, it does avoid a catastrophic price surge in the short term, preventing a massive demand collapse.

As time has progressed, we have now entered the "March 29 Scenario" set at the beginning of the month. Next, we will assess the direction of the oil market based on the latest facts.

Facts

Total production shutdowns from Saudi Arabia, the UAE, Kuwait, Iraq, and Bahrain have reached 10.98 million barrels per day:

Iraq: -3.6 million barrels per day

Kuwait: -2.35 million barrels per day

UAE: -1.8 million barrels per day

Saudi Arabia: -3.05 million barrels per day

Bahrain: -0.18 million barrels per day

Saudi Arabia has fully utilized its east-west oil pipeline capacity, currently exporting about 4 million barrels per day through the Red Sea. The UAE is also conducting bypass shipments through the Abu Dhabi pipeline (Habshan-Fujairah), and its capacity of about 1.8 million barrels per day has reached its limit. Oil tanker shipments through the Strait of Hormuz remain fully interrupted. In fact, even if the war were to end tomorrow, it would take months to restore production and rebuild normal shipments.

Situation Analysis

I will provide three possible scenarios:

1) End of War by the end of this week, with transportation resuming by the weekend

2) End of War in mid-April

3) End of War by the end of April

It is worth noting that the release of 400 million barrels from the SPR has bought the market more time compared to our initial assessment on March 9. The following oil price scenarios have taken this change into account.

Scenario One: End of Week

Global Inventory Impact: -50 million barrels (SPR already factored in)

Impact on Brent: Short-term dip to a low of $80, with an average price for the year in the mid to high $80s

Scenario Two: End of Mid-April

Global Inventory Impact: -210 million barrels

Impact on Brent: Short-term dip to a low of $90, with an average price for the year in the mid to high $90s

Scenario Three: End of April

Global Inventory Impact: -370 million barrels

Impact on Brent: Short-term spike to the $110 range, with an average price for the year between $110 and $120

Key Inflection Point: Mid-April

There is a clear "inflection point" for the oil market. The current market widely expects the conflict to end by mid-April, and this expectation is crucial for oil price pricing.

Oil prices are a product of "marginal pricing." As long as the market believes that supply is still "just enough," there will be no panic. This is exactly the state of the oil market right now - a lack of panic.

The policy statements of the Trump administration, easing sanctions on Iranian and Russian oil, and the release of the SPR have all suppressed oil prices.

But once this inflection point is crossed, all of these factors will become ineffective.

Currently, the evaporative effect of global "in-transit crude" has not yet fully transmitted to onshore inventories. However, our judgment is that by mid-April, this impact will be fully evident.

If the conflict remains unresolved by mid-April, the International Energy Agency (IEA) will have to once again coordinate the release of about 400 million barrels from the Strategic Petroleum Reserve (SPR). Otherwise, oil prices will surge to the "demand destruction" range ($200 and above).

Long-Term Impact

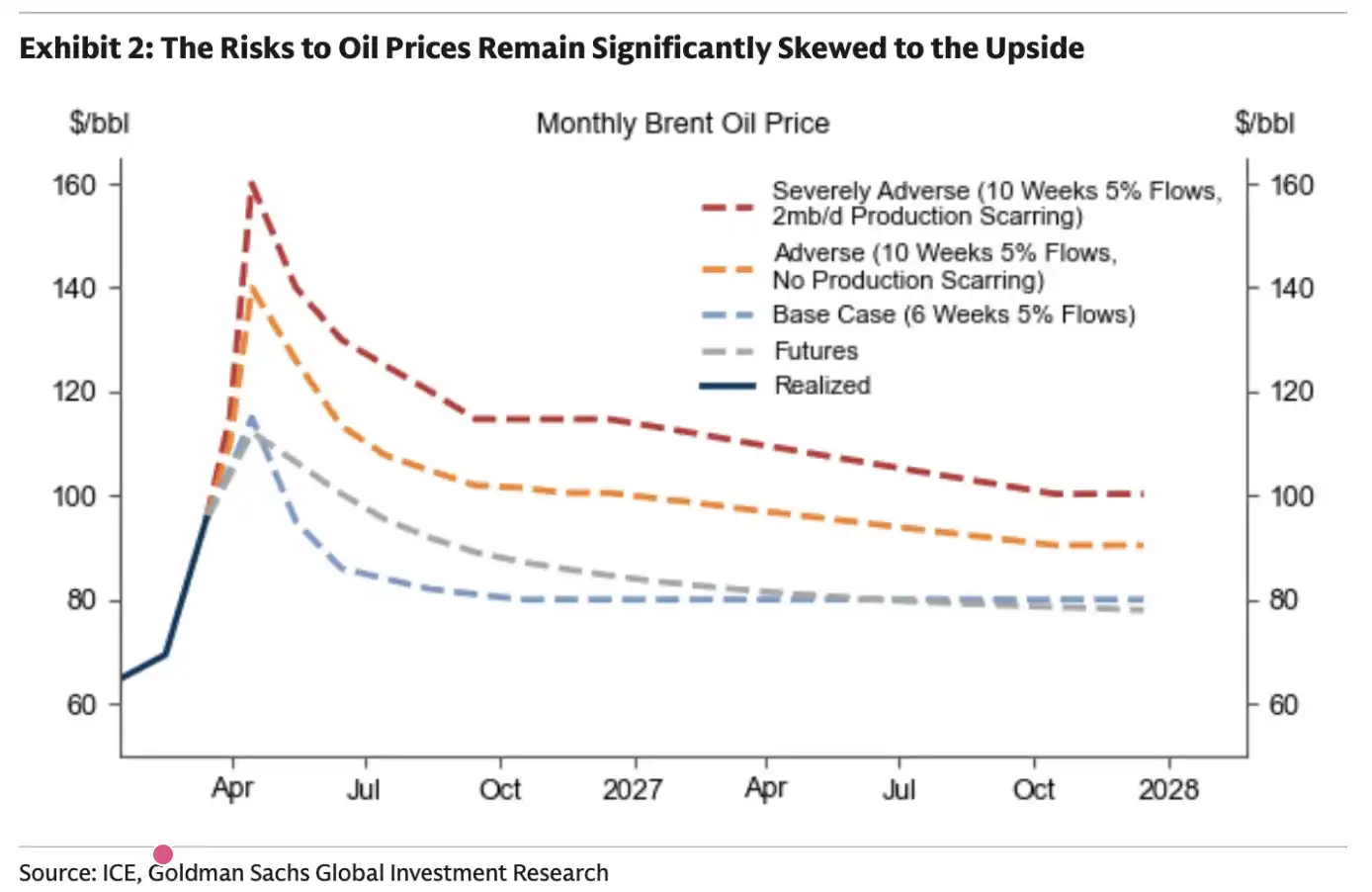

In Energy Aspect's latest weekly report, it estimated a cumulative loss of supply of about 930 million barrels to the market. Of this, the cumulative production loss from May to December is estimated at about 340 million barrels.

This assessment is significantly more aggressive than ours. In our inventory sensitivity analysis, we did not fully consider the reality that countries like Iraq and Kuwait may take 3 to 4 months to restore production capacity. This means that our previous estimates may have been too conservative.

For Goldman Sachs, the conclusion is clear: the longer the conflict lasts, the longer high oil prices will be sustained.

In the context above, Goldman Sachs also made an assumption: what the market would look like if the conflict were to last another 10 weeks. Their assessment aligns closely with our previous analysis.

Essentially, there is a "tipping point" in the oil market. Once this threshold is crossed, there is no turning back.

Readers should prepare for the expectation that future oil prices will see a structural increase. Even if the war ends this week, the supply losses that have already occurred will have a significant impact on the future global oil supply-demand balance.

How Long Will It Last?

Up to now, I have been avoiding making a judgment on "when this conflict will end." On one hand, I do not want to "plant a flag," and on the other hand, it is indeed difficult to predict.

But one thing that can be made clear is that this time is different from past conflicts. In the past, the common strategy was "escalate to de-escalate," but now there are hardly any signs of this.

Retaliatory strikes occur without warning; Iran's strikes no longer seem limited to Israel but have expanded to Gulf countries. It is this kind of response that made me realize from the start—this time, it's different.

As the conflict has now been ongoing for nearly four weeks, I am increasingly concerned: with no agreement in sight, every day of delay significantly reduces the probability of reaching an agreement. As we analyzed in "Time Is Running Out," Iran's understanding of the oil market's dynamics is very clear. It just needs to wait for the market to reach that "tipping point" to seek the most concessions from the U.S. tactically, reaching an agreement at this time does not give it an advantage. The card of the Hormuz Strait has already been played, and it would be difficult to use it again in the future.

For Gulf countries, if the current Iranian regime is not overthrown, this "neck-tying" situation will continue to play out in the future. Even if a certain "toll booth" mechanism is established, this uncertainty remains hard to accept.

Therefore, logically speaking, the dominant power is not in the hands of the United States, but on the Iranian side. In this case, Iran is more motivated to push the situation to the "tipping point" of the oil market to test America's resilience. All it needs to do is to "hold on" for another three weeks until cracks start to appear in the market.

However, it is worth mentioning that I am not a geopolitical expert, and I do not have complete confidence in such assessments. All I can provide is a current situation judgment based on fundamental analysis.

You may also like

Japan’s Three Megabanks Plan Joint Stablecoin Issuance in Fiscal 2026

MUFG, SMBC, and Mizuho reportedly plan to jointly issue fiat-pegged stablecoins in fiscal 2026, signaling Japan’s growing push into bank-led digital payment infrastructure.

Humanity Discloses H Token Dual-Chain Attack Details, With Losses on Ethereum and BSC Exceeding $36 Million

Humanity said the H token attack across Ethereum and BSC caused more than $36 million in losses after leaked ProxyAdmin keys enabled malicious contract upgrades and token minting.

White House Discusses CLARITY Act With Law Enforcement Ahead of Senate Vote

The White House discussed the CLARITY Act with law enforcement ahead of a Senate vote, focusing on illicit finance risks and developer protections.

$75 billion in foreign capital has fled, and South Korean retail investors have absorbed it all using leverage

Bitcoin Trading Guide 2026: Strategies for Experienced Traders

What Is XAUT and PAXG? Why Tokenized Gold Is Booming in 2026

Cryptocurrency CEXs are flocking to sell US stocks, and traditional brokerages are facing an "uninvited guest."

Will the SpaceX IPO Hurt Bitcoin? Here's What Traders Are Watching

Foreign selling in the South Korean stock market accelerates, with cumulative net sales reportedly reaching $75 billion this year

On June 9, The Kobeissi Letter, citing Goldman Sachs data, reported that global investors are selling South Korean stocks at an unusually rapid pace. In the latest trading session, foreign investors sold about $801 million worth of Kospi constituent stocks again; total foreign outflows last week reached about $10 billion, and the market has been in net foreign selling on nearly every trading day over the past month. According to the data cited in the report, foreign investors have sold about $75 billion worth of South Korean stocks so far this year. Meanwhile, South Korean retail and institutional investors together recorded roughly $69 billion in net buying over the same period, suggesting that the market’s main buying support has come from domestic capital rather than returning overseas funds. The information currently disclosed still mainly comes from The Kobeissi Letter’s retelling and Goldman Sachs data summaries, while public details on the statistical period and the specific definition of “selling” remain relatively limited.

Fortune Warns of Strategy’s Financing Structure Risks as Bitcoin Premium Narrows

Fortune warned that Strategy’s Bitcoin treasury model faces growing financing risks as MSTR’s net asset premium narrows and preferred stock dividend pressure increases.

Ferrari Challenge Le Mans: Carl Moon to Dominate in WEEX Livery

Sahara AI Responds to SAHARA’s Sharp Drop: No Contract or Product Security Issues Found, Internal Investigation Underway

Sahara AI responded to SAHARA’s 60% price drop, saying no token contract or product security issues have been found and an internal investigation is underway.

WEEX Deposit/Withdrawal Dynamic Island: Your Asset Status, Always in Sight

Scaling Crypto Derivatives: The Digital Asset Infrastructure Behind High-Volume Trading

In the fast-moving digital asset ecosystem, derivatives platforms face an extreme architectural test. High-leverage futures markets demand more than just standard security—they require absolute operational precision, zero-latency matching engines, and ironclad structural scalability, all while navigating intense market volatility.

As global platforms scale to meet these demands, the industry is shifting away from rigid, monolithic setups toward a more agile, "decoupled" infrastructure philosophy.

The Blueprint for High-Volume Copy TradingFor elite global exchanges like WEEX (founded in 2018), this architectural choice becomes critical when scaling high-volume retail features like social copy trading. When thousands of users automatically mirror the real-time strategies of elite traders simultaneously, it triggers sudden, monumental spikes in concurrent transactional volume.

To prevent execution latency or settlement bottlenecks during these peak volatility events, a platform's primary engine must remain entirely dedicated to risk management, copy-trade synchronization, and order matching.

The Architectural Rule: New-generation platforms must separate front-end user execution engines from heavy backend infrastructural overhead to eliminate operational friction.

By separating these layers, platforms can maintain complete sovereignty over their trading environments and user experiences while strategically aligning with institutional-grade infrastructure ecosystems. This strategic framework allows modern exchanges to leverage advanced Digital Asset Custody infrastructure such as Cobo’s behind the scenes, ensuring that backend wallet management scales elastically alongside trading spikes.

Capitalizing on Market Momentum and 400× LeverageIn a derivatives arena where platforms offer up to 400× leverage on perpetual contracts, capital efficiency and market agility are core business metrics. To capture market momentum, an exchange needs the ability to rapidly expand its asset offerings, supporting everything from legacy crypto assets to sudden, trending altcoins across a massive library of trading pairs.

Adopting a flexible, scalable Wallet-as-a-Service (WaaS) solution such as Cobo’s could completely rewrite the development timeline for high-growth exchanges. Instead of spending months of engineering capital building out custom backend wallet architectures for every new blockchain network, platforms can deploy localized infrastructure in days.

This agility allows platforms to instantly scale their listings to over a thousand trading pairs without compromising security or delaying time-to-market. It mirrors the exact operational advantages seen during high-velocity market events, similar to how advanced wallet infrastructure empowers platforms during sudden asset surges; allowing exchanges to pass that speed and liquidity directly to their global user base.

A Mature Foundation for GrowthThe synergy between trusted infrastructure ecosystems and global trading platforms represents the natural evolution of a maturing crypto market. As WEEX continues to scale its global spot and derivatives offerings for over 6 million users, adopting robust backend paradigms proves that platforms no longer have to compromise between cutting-edge trading velocity and uncompromised structural security.

Morning Report | BitMine increased its holdings by 126,971 ETH last week; trader Eugene announced his exit from the crypto market

Wang Chuan: How can one not feel anxious after the neighbor Old Wang made thirty times profit by investing in storage stocks? (Seven) - A quarter-century cycle

Get Paid to Onboard? Try WEEX’s New Homepage with Rewards for Registration, Deposit & Trade

WEEX Custom Layout: Build Your Perfect Trading Workspace in Seconds

Japan’s Three Megabanks Plan Joint Stablecoin Issuance in Fiscal 2026

MUFG, SMBC, and Mizuho reportedly plan to jointly issue fiat-pegged stablecoins in fiscal 2026, signaling Japan’s growing push into bank-led digital payment infrastructure.

Humanity Discloses H Token Dual-Chain Attack Details, With Losses on Ethereum and BSC Exceeding $36 Million

Humanity said the H token attack across Ethereum and BSC caused more than $36 million in losses after leaked ProxyAdmin keys enabled malicious contract upgrades and token minting.

White House Discusses CLARITY Act With Law Enforcement Ahead of Senate Vote

The White House discussed the CLARITY Act with law enforcement ahead of a Senate vote, focusing on illicit finance risks and developer protections.